Dubai: India’s gold jewellery manufacturers are seeking more than a helping hand from Dubai’s precious metal trade in what is being seen by some industry insiders as a “fight for survival”.

An Indian industry grouping – Indian Jewellers of Excellence, which represents more than 70 businesses – is holding a two-day B2B summit here to showcase their handcrafted merchandise and designs and expecting to generate interest from local retailers. The organisers are hopeful that jewellery retailers from other Gulf states would also come calling and place orders.

“Only by getting export orders – ideally from the multi-chain retailers here and elsewhere in the Gulf – can India’s jewellery manufacturers expect some relief from the crisis in India,” said P. V. Jose, director at Indian Jewellers of Excellence.

India’s jewellery retail is off by 40 per cent as Indian authorities kept raising the cost of buying. There is now a Rs300 difference on each gram of gold sold in India and its equivalent rate in Dubai.

In sync with the retail demand drop, jewellery makers in India have also seen a 40 per cent decline in their recent off-take domestically. The decline in the rupee has only compounded their long list of concerns.

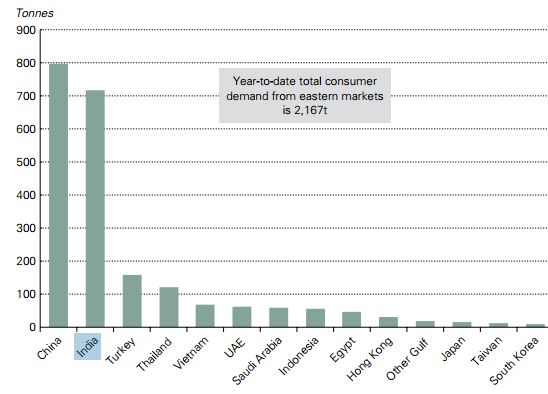

As of now, more than 90-95 per cent of the gold jewellery processed in India is sold within that market itself. Now, the Indian government wants Indians to reduce their fascination with the metal and reduce its imports to keep a curb on the current account deficit.

What they have done is raise the import duty on bullion to the level of 10 per cent now and also placed demands on metal buyers to make sure they sell 20 per cent of their off-take in overseas markets.

So, from being singularly focused on the domestic selling, India’s jewellery makers are forced to shift their gaze elsewhere. The Gulf is an obvious destination to press their designs, and they will also have roadshows in the Far East.

“There are certainly opportunities for Indian jewellery makers to present their case with distributors and retailers,” said Sunny Chhittilappilly, who heads the Dubai Gold and Jewellery Group. “A major advantage for both is the weakness of the rupee vis-à-vis the dirham/dollar. Retailers here could offset some of the higher costs of local sourcing by placing orders on specific designs or collections with makers in India.”

(However, it must be noted that the leading local and GCC based retailers already have their own jewellery making operations.)

But to get to the 20 per cent export levels will be daunting, at least initially. The 70-odd manufacturers process 400-500 kilos a day and which peaks to 1,000 kilos during the key buying seasons.

“The Indian government is pushing us to seek overseas markets, but they have not offered any tax breaks or other incentives,” said Jose. “Gold is embedded in the culture of India and has been so for 6,000 years. To try and make changes in culture overnight is impossible.

“If they wanted to reduce dollar outflow, why aren’t they doing something about the flood of Chinese-made mobile phones – 250 million handsets a year – coming into the country or of luxury vehicles? Why not place restrictions on a product such as a mobile which does not have a value beyond six months?”